Here it is for you non-resident tax payer

theRIPregistry

Looking to buy a property?

MAY 09, 2019

Do you need mortgage insurance?

By Helen Burnett-Nichols

Your home is likely the biggest asset you’ll ever own. So how can you protect it in case something were to happen to you?

Canadians owe $2.17 trillion in household debt, according to the Bank of Canada. More than 70% of that is residential mortgage debt. To protect these mortgages, homeowners have a couple of options. You can buy mortgage insurance from a financial institution. Or you can get mortgage protection with life insurance and critical illness insurance from an insurance company.

- Mortgage insurance works by paying off the outstanding principal balance of your mortgage, up to a certain amount, if you die.

- Mortgage protection, on the other hand, uses a combination of insurance policies to protect you:

- Term life insurancecovers you for a set period, such as 10, 15, 20 or 30 years. It can be suitable if you’re looking for low-cost insurance. While the premium may be low for the first term, the cost will increase when it’s time to renew. Buying coverage for a long enough term to match your mortgage term – 30 years, for example – will keep the cost steady. (Read more: Is term life insurance right for you?)

- Permanent life insurancecan be more expensive at first, but it covers you for life. The amount you pay can either be guaranteed to stay the same or vary over time, depending on the type of plan you choose. (Read more: Is permanent life insurance right for you?)

- Critical illness insurance gives you a one-time payment if you are diagnosed with a serious illness that’s covered under the policy (and you meet the other policy conditions). You can use the money for medical expenses, to pay off your mortgage or for anything else you wish – it’s up to you. (Find out how a serious illness could affect your finances. Try this Critical illness insurance calculator.

Key differences between mortgage insurance and mortgage protection with life insurance and critical illness insurance

The main difference with mortgage insurance is that the payment goes to the lender. The amount you’re covered for declines as your mortgage balance declines. With mortgage protection, critical illness insurance gives you a one-time payment you can use for your mortgage or other expenses as you choose. And life insurance pays a tax-free amount to your chosen beneficiary (the person who receives the benefit) when you die. The payment can cover more than just the mortgage. The beneficiary may use the money for any purpose.

Beneficiary. With mortgage insurance, the money goes to the lender. With critical illness insurance, the money goes to you. With life insurance, it goes to whomever you name as the beneficiary.

Portability. If you change mortgage providers, your mortgage insurance doesn’t automatically move with you. If you move your mortgage to another lender, you’ll have to prove that your health is still good. You’ll also pay the mortgage interest rate the new mortgage provider offers. With life and critical illness insurance, you can take your policy with you if you transfer your mortgage to another company. There’s no need to re-apply or prove your health is good enough to be insured.

Flexibility. With mortgage insurance through a lender, your needs may change over time. But you don’t have the flexibility to change your coverage. With mortgage protection, you can convert term life insurance and term critical illness insurance plans into permanent plans later on.

OWN A HOME? Do you pay your mortgage down or contribute to your RRSP?

What do you do? Find out more. Check out this calculator.

https://www.sunware.ca/illustrations/savings.aspx?isRecalc=N&selectedLanguage=en-CA

Student Forgiveness Loans!

I FOUND THIS SITE AND THOUGHT IT MIGHT BE OF INTEREST TO MANY OF US… FIND OUT HOW TO GET STUDENT LOAN FORGIVENESS. A MUST READ!

YOUR GUIDE TO CANADA STUDENT LOAN FORGIVENESS

See below for credits

Student loan debt is a big problem in Canada, and it’s not going away any time soon. The average new graduate is carrying $28,000 in student loan debt. Pair that with high housing costs and low wages, and it’s no surprise that most millennials are putting off major life milestones because they simply can’t afford it.

There is a small glimmer of hope for those struggling with provincial and federal student loans, and it comes in the form of student loan forgiveness. I took advantage of New Brunswick student loan forgiveness when I wiped out $16,000 of my $42,000 in student loan debt. Without that loan forgiveness program and others like it, there’s no way I could have paid off $38,000 in two years.

If you’re one of the many young Canadians dealing with high student loan debt, I’ve put together a list of possible resources for you to tap to reduce your debt burden. Before you jump to your province and start going click happy, there are a few things you should know:

First, most of these programs are only for publicly funded student loans. If you have loans through a private lender, skip to the bottom of this blog post for additional resources.

Second, every province has a repayment assistance program (RAP). A RAP is there if you can’t make your minimum student loan payments. It’s not student loan forgiveness, it’s just there to help you if you are having trouble earning enough money to make your minimum payments. I’ve listed a few of them below.

Finally, some of these programs are applied to your loan automatically and some aren’t. Read the fine print on every website and mark the due dates on your calendar so you don’t miss out on your chance to reduce your student loans just because you didn’t get your application in quickly enough.

Enjoy!

FEDERAL CANADA STUDENT LOAN FORGIVENESS

Canada Repayment Assistance Plan (RAP)

The Canada RAP program is useful for university graduates who are having trouble paying their student loans back. The program makes it easier to manage your student loans by reducing the amount you have to pay each month or eliminating all together.

Canada Student Loan Forgiveness for Doctors and Nurses

If you’re a doctor or a nurse you can qualify for loan forgiveness for your Canada student loans by working in a remote or rural area. If you are a doctor, you could qualify for up to $40,000 in loan forgiveness over five years ($8,000 per year). If you’re a nurse you could qualify for up to $20,000 in Canada student loan forgiveness over five years ($4,000 per year).

BRITISH COLUMBIA STUDENT LOAN FORGIVENESS

Full-time students who successfully complete a year of studies may have the B.C. portion of their B.C.-Canada student loan debt reduced. There is not need to apply for this grant, you are automatically considered if you have a B.C.-Canada student loan.

B.C. Completion Grant for Graduates

A $500 grant for graduates from an undergraduate program. You must have a B.C. student loan and you must apply within one year of graduation.

Recent graduates in select in-demand occupations can have their B.C. student loans forgiven by agreeing to work at publicly funded health care facilities in underserved communities in B.C., or working with children in occupations where there is an identified shortage in B.C.

Pacific Leaders Loan Forgiveness Program

This program forgives outstanding B.C. student loan debt at a rate of one third per year. If you continue to work for the B.C. Public Service for three years, your B.C. student loan will be paid off in full.

ALBERTA STUDENT LOAN FORGIVENESS

Alberta Repayment Assistance Program (RAP)

Similar to the Canada RAP program, the Alberta RAP helps graduates who are struggling to make their monthly payments. This program reduces or eliminates your student loan payments. You have to reapply every six months.

SASKATCHEWAN STUDENT LOAN FORGIVENESS

Saskatchewan Repayment Assistance Program (RAP)

Saskatchewan also has a repayment assistance program if you are having trouble making your monthly payments. This program limits your monthly payments to no more than 20% of your gross income.

The Graduate Retention Program provides Saskatchewan income tax credits of up to $20,000 for tuition fees paid by graduates who live in Saskatchewan. To be eligible you need to live and file your income tax return in Saskatchewan. The tax credits are non-refundable.

Loan Forgiveness for Nurses and Nurse Practitioners

This program encourages nurses and nurse practitioners to work in rural and remote communities. You can use this program to receive $4,000 per year up to a maximum of $20,000. You must have a Saskatchewan student loan to qualify.

MANITOBA STUDENT LOAN FORGIVENESS

Repayment Assistance Program (RAP)

Surprise! Manitoba also has a repayment assistance program.

ONTARIO STUDENT LOAN FORGIVENESS

There are 12 grants and bursaries available to students with Ontario student loans. Most of them only apply to you if you are currently a student. You must have Ontario student loans to qualify.

QUEBEC STUDENT LOAN FORGIVENESS

A version of RAP, the deferred payment plan allows you to pay back your student loans in accordance with your income. The deferred payment plan can be applied to a variety of financial institutions, not just provincial student loans.

NOVA SCOTIA STUDENT LOAN FORGIVENESS

0% Interest on Nova Scotia Student Loans

If you live in Nova Scotia, filed your income tax in Nova Scotia and have Nova Scotia student loans since 2007, you can apply for 0% interest on the provincial portion of your student loans. Your monthly payment will remain the same but 100% of your payment will go to your loan principal.

Nova Scotia Student Loan Forgiveness Program

This program is for Nova Scotia student loans (not federal student loans) issued after August 2015. You must be a Nova Scotia resident obtaining a four-year degree at a Nova Scotia university to qualify. You are automatically assessed for this forgiveness program, which can forgive up to 100% of your Nova Scotia student loan.

The debt cap program applies to students who received Nova Scotia student loans between August 1st, 2011 and July 31st, 2015. Anyone who obtained a four-year undergraduate degree qualifies. You are automatically assessed for this program when you graduate. You could have up to 100% of your Nova Scotia student loans forgiven.

Anyone who received student loans between August 1, 2003 and July 31, 2008 can apply for Nova Scotia’s debt reduction program. You must have successfully graduated from your degree program to apply.

NEW BRUNSWICK STUDENT LOAN FORGIVENESS

The timely completion benefit is available for students with New Brunswick student loans who graduated from a four-year undergraduate program after August 1, 2009. You must have a total federal and provincial student loan amount totaling more than $32,000 and you must apply within seven months of graduation.

PRINCE EDWARD ISLAND STUDENT LOAN FORGIVENESS

Receive up to $2,000 per year of study, as long as you take out at least $6,000 per year in student loans. You must have PEI and Canada student loans to qualify and you must apply within 60 days of your last day of class.

NEWFOUNDLAND STUDENT LOAN FORGIVENESS

Newfoundland and Labrador Debt Reduction Grant

With the elimination of the Newfoundland Student Loan, all financial assistance from the province is in the form of a non-repayable NL Student Grant effective August 1, 2015. If you receive provincial funding after August 1, 2015 you will be automatically assessed for this grant.

This may not be an exhaustive list. If you know of other programs that aren’t listed here, or if any of these programs have expired, I encourage you to email me and let me know so I can keep this list up to date.

If you’ve already applied for all of the grants you qualify for and you still have student loan debt left (as I did), the next step is to pay it off. I encourage you to use my debt repayment spreadsheet to find out how quickly you can pay off your debt.

Most of the programs listed above are only available for federal and provincial student loans. If you have your student loans with a private lender, you won’t be able to use the programs above. If that is the case, consider looking into student loan refinancing as a possible way lower your interest rate and pay off your debt quicker.

posted March 9, 2016 from https://myalternatelife.com/canada-student-loan-forgiveness/

What Federal and Provincial Benefits do seniors get in Ontario?

- Federal benefits.

- Canadians living and working in Ontario are likely eligible for Canada Pension Plan (CPP) benefits at retirement. At age 60 you may apply for a permanently reduced amount, or defer to after age 65 for an increased pension.

- Find retirement homes in Ontario.

Privately owned and funded entirely by resident fees, these 55+ communities are designed for seniors who do not have significant mobility or medical issues. Retirement Communities provide a variety of social, culinary, fitness and support services to all residents, who enjoy a relaxing and maintenance-free lifestyle. Shared accommodation, private condos, or cottage-style residences are all available to select from. -

Ontario is a premium retirement destination for many Canadians – thanks to a thriving economy, modern medical and financial infrastructures, and moderate weather. Over 12 million residents reside in the province, with seniors constituting 14.2% of this population. The province’s largest city is Toronto, which is situated on the shores of Lake Ontario. Home to over four million, 12.4% of the city’s population are senior citizens – a number that’s slated to grow to 20%+ by 2036. - Canadian residents may apply for Old Age Security (OAS) at age sixty-five. To be eligible you must have resided in Canada for a minimum of ten years as an adult (18 years of age and up). Your employment history is not a factor in determining eligibility. .

- International benefits, made possible due to social security agreements, are available to Canadians living outside Canada, but who have previously been a resident of Canada for twenty years. If you are a survivor of an individual that has worked in Canada and internationally, you may also be eligible

- Guaranteed income supplement (GIS)

Low-income Canadian residents receiving OAS, may be eligible to receive a Guaranteed Income Supplement. Your household income must be within preset parameters. Note: Beginning in April 2023, the eligible age for OAS and the GIS will increase from age 65 to age 67 over a six-year period with full implementation by Jan 2029. Those affected were born on or after April 1, 1958. - Allowance program.

If you are age 60 – 64, a legal resident and citizen of Canada, having lived in Canada for 10 years since age 18, and your spouse or common-law partner is receiving OAS and GIS, you may be eligible for an allowance benefit – your household income will be considered for eligibility. If you have not lived in Canada for 10 years but your country of residence has a social security agreement with Canada, you may be eligible for a partial benefit. - Allowance for the survivor

If you earn a low income and have lived in Canada and your spouse or common-law partner is deceased, you may be eligible for the Allowance for Survivor benefit. To be eligible you must be age 60 – 64, be a Canadian citizen or legal resident, and lived in Canada for at least 10 years after age 18. This allowance will stop at age 65 when you may be eligible for OAS and a GIS.

Who Needs This? Do you?

Most people don’t know they need this! Only 3 slides tells a story

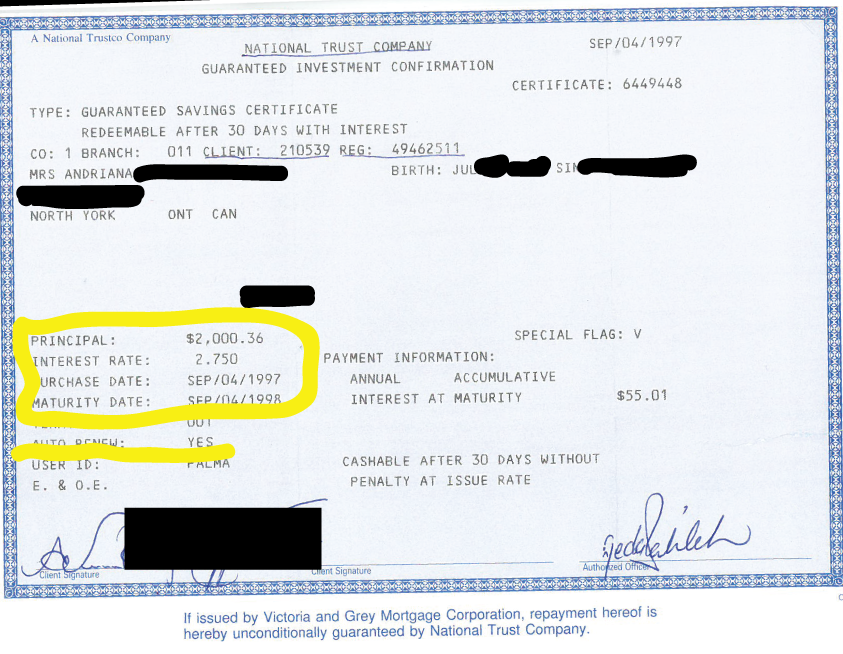

National Trust GIC of $2000.36 lost with acquisition of Scotia Bank

This is my story.

To say that I am disappointed is an understatement. I am a mother of twin girls. As I am getting older I decided to get my affairs in order and document everything at theRIPregistry.com. I went to my safety deposit box and found a National Trust Company GIC which was purchase on September 4, 1997. It was supposed to have auto renewed annually. The GIC certificate ($2000.36 at 2.75%) along with bonds purchased were placed in a Safety Deposit box for safe keeping and to be redeemed when the time came. The plan was to put money aside in order to grow and eventually be used towards their education towards university cost. Today 2018, my kids are older and both are in university. I contacted Scotia Bank who acquired (bought-out) National Trust back in August 1997. Scotia (office of the president) apologized and said “this GIC was too old” they further told me they keep their records for only 7 years under the government rules and that they found nothing and there was nothing they can do”.

Their research of my GIC renewal certificate included checking the Bank of Canada to see if it was transferred over to them. This GIC was purchased after they announce the acquisition of National Trust and now they seem to be pointing the finger everywhere else. It is important to note that the Bank of Canada only accepts funds from accounts that had been dormant and unclaimed (this would be savings and chequing accounts). What I purchased was a GIC and had it set for auto renew, therefore the chances of it becoming dormant was NIL. To insult me stating they checked the Bank of Canada to see if it was in their hands was disappointing and to further blame their client (me) stating that it had to have been cashed is distasteful.

The GIC certificate has my birth date, my SIN and had my sister’s home address. Life moved on and I ended up in the hospital several times. My kids being 2 months premature were in and out of the hospital and life was hectic with the girls. Therefore to say that I at some point cashed in this GIC investment which was set for auto renew is absurd. $2000.36 amounts to quite a bit of money after 20 years of renewing at the higher interest rate.

If The RIP Registry (theRIPregistry.com) was available 20 years ago, I don’t believe this GIC would have been lost. The RIP Registry is an on-line tool that would be visited frequently as life goes on when deciding to purchase, life insurance or disability insurance. It is useful to document your vehicle, home and land purchases, business ventures, partners, loans given or borrowed. You may have purchased life or disability insurances or antiques, jewellery, storage units etc. What if along the way, as many of us have, decided to purchase RESPs (Educational Savings Plans) maximizing the government grants for your children. With The RIP Registry (theRIPregistry.com) you would be able to document your progress and built up products in your portfolio at theRIPregistry.com easily and at no cost (Abolutely Free). Its accessible anywhere any time.

Looking back at what I lost & forgotten, I can honestly say that you have to take care of your own destiny and finances by visiting your investments, mortgages, products etc. annually and keeping it fresh in your mind. Trusting the Banks, your investors or insurance companies, in my opinion, is not the way to go. They all say they have your best interest at heart and are working for you, but are they? It’s all about money and what you can do for them. Remember no one will take care of YOU or what you have worked so hard for, like YOU will. In case of floods, fires or you just can’t remember where you have what and where, The RIP Registry is an online tool that can help, it’s SECURE and it’s FREE!, Sign up at theRIPregistry.com.

Elderly Couple Lost $300,000

November 28, 2018

Financial, Insurance, Planning, theRIPregistry, Uncategorized

She worked all her life for her retirement and build a nest egg and future for her and her family.

This happens all to often, but we are unaware and go thru life not giving it a second thought. If you have been an executor have you considered or even thought what could be missing and all the work involved. This registry keeps it organized and its simple.

Just print a Go-To Report and use it as your checklist. It’s easy and gives you and your loved ones peace of mind when the unexpected happens. The RIP Registry is FREE and a necessary tool to help you and it’s FREE.

Sign up at theRIPregistry.com and get your ducks in a row!

Why The RIP Registry?

In today’s world there is so much happening and we are rushing thru life at record speed. We want to ensure we build a portfolio for our retirement and to leave a legacy behind, when the time comes. I felt a need to create this for myself and soon realized, I’m not alone and there is a general need for a registry like this. It all started with my dad going to the hospital and having to drop everything to take care of my aging sick mother.

ENERGY & FOOD – Aid and Support for your loved ones!

Energy

The Ontario Energy Board’s Low Income Energy Assistance Program (LEAP) provides low-income customers up to $500 in emergency financial assistance to pay their gas or electricity bills ($600 if their home is heated electrically). Low-income Enbridge customers can apply for the Home Winterproofing Program. Enbridge also offers the Community Energy Conservation Program in some parts of Ontario, which brings with it incentives of up to $2,000 to qualified homeowners.

Food

Call 2-1-1 to find agencies which provide grocery shopping rides, to find Meals on Wheels or food banks if you or your loved one are mobile. Some municipalities, such as Toronto, operate Good Food Box programs, which deliver boxes of affordable, fresh produce to pick up locations on a regular basis. Call 2-1-1 to find out what food or meal programs are available near you. Help With Pet Costs

Dogs or cats are essential to the wellbeing of many seniors, but paying for their expenses can be worrisome if money is tight, especially if they fall ill. If you don’t have enough money to pay vet bills, you might be eligible for help from the Farley Foundation.

If you or your loved one is in need of more information on financial assistance for seniors, call 2-1-1 Ontario at any time to speak with us about an individualized plan to help minimize your financial concerns and allow you to age without boundaries!

more at #seniorsforseniors

Follow & like us on https://twitter.com/theripregistry; https://www.facebook.com/

____

It is important to document their legacy (whatever that may be) for when the time comes. You don’t want your last memories to be one of stress and searching and planning. theRIPregistry.com will help you or your loved ones keep organized. It is a go to check list for when the time comes ensuring you keep your legacy where it matters.

Listen to the many stories how the system can fail us. We pay into insurances, investments and into our portfolio, building a legacy only to one day have it lost or unclaimed.

Check our first blogs where you will find stories of unclaimed monies, safety deposit boxes and more

- Elderly Couple Lost $300,000

- National Trust GIC of $2000.36 lost with acquisition of Scotia Bank

- Vehicle Repossessed

Recent Comments